Understanding SOFE Certification Exams: A Complete Introduction

Getting your SOFE certification isn't something you just breeze through on a Tuesday afternoon. The Society of Fire Protection Engineers runs these exams, and they're designed to separate people who actually know fire protection engineering from those who just think they do.

The certification process tests real competency. Not the kind you get from skimming a textbook the night before, but the deep understanding that comes from actually working with fire protection systems and knowing what happens when things go wrong.

SOFE offers different certification paths depending on where you are in your career. Fresh graduates take one route. Experienced professionals take another. The exams adjust their focus based on what you should reasonably know at each stage. A five-year veteran gets grilled on things an entry-level engineer hasn't encountered yet.

Most people spend months preparing. The exam covers fire dynamics, suppression systems, detection technology, building codes, and risk assessment. You need to understand how these elements interact in real buildings with real occupants. Theory matters, sure, but so does practical application.

The study materials SOFE provides are full. Some might say exhaustingly so. You get reference guides, practice problems, and sample questions that mirror the actual exam format. Many candidates join study groups because going it alone can feel like trying to drink from a fire hose. The irony isn't lost on anyone.

What throws people off is the scenario-based questions. You don't just regurgitate definitions. Instead, you analyze situations, identify hazards, and recommend solutions. The exam wants to see your thought process, not just your memory.

Pass rates vary by certification level. Entry-level exams see higher pass rates than advanced certifications. Makes sense when you consider the complexity increases substantially as you move up. Nobody said fire protection engineering was easy.

The testing environment is controlled and proctored. You can't phone a friend or consult your favorite engineering handbook mid-exam. It's you, the questions, and whatever you managed to cram into your brain during preparation.

Some candidates take the exam multiple times. There's no shame in that. The material is really difficult, and sometimes you need a practice run to understand what you're up against. Each attempt teaches you something about the test structure and your own knowledge gaps.

After you pass, maintaining certification requires continuing education. Fire protection technology doesn't stand still. New materials, updated codes, and emerging research mean what you knew five years ago might be outdated today. SOFE wants certified engineers who stay current.

The certification carries weight in the industry. Employers recognize it. Clients trust it. It signals you've met a standardized measure of competence that goes beyond whatever degree is hanging on your wall.

Preparing for SOFE exams demands discipline. You can't cram everything the week before and expect success. The knowledge base is too broad and the application too nuanced. Successful candidates typically follow structured study plans spanning several months.

Understanding the exam format helps. Multiple choice questions dominate, but they're not simple recall items. Each question requires analysis and sometimes calculations. Time management during the exam matters almost as much as knowing the content.

The investment of time and money is significant. Between study materials, exam fees, and the hours spent preparing, you're looking at a real commitment. But for serious fire protection engineers, it's the credential that defines professional standing in the field.

Look, if you're working in financial regulation or thinking about it, you've probably heard about SOFE Certification Exams. They're not as famous as the CPA or CFA, but in the regulatory world? They matter a lot.

The certification space's overwhelming. When you're just starting out, it feels like there's a hundred different acronyms to chase, each one promising to unlock some career door you didn't even know existed. But SOFE credentials? Actually pretty focused compared to those monster exams that swallow years of your life.

The organization behind the credentials

The Society of Financial Examiners exists for one main reason: making financial regulation better through professional development. Not some huge corporate entity. It's a professional organization that state insurance departments, federal regulators, and people working in financial institutions actually use for career growth and networking.

SOFE was founded to promote excellence in financial examination practices. What does that mean in practice? They set standards for what a competent financial examiner should know and how they should behave ethically. They run conferences where examiners from different states swap war stories and learn about new examination techniques. Wait, I'm getting ahead of myself here. They also provide continuing education so people don't get stuck using 1995 methods in 2026, which honestly would be a disaster given how much has changed.

The membership benefits? Pretty solid if you're in this field. You get access to networking events where you can meet examiners from other jurisdictions. Useful when you're trying to figure out how other states handle tricky situations. Career resources, technical publications, and yeah, the certification programs we're here to talk about.

My cousin works for a state insurance department and swears by these networking events. Says he's learned more troubleshooting weird cases over hotel conference room coffee than from any manual. Sometimes the unofficial channels teach you more than the official ones.

Why these certifications actually exist

SOFE certification programs validate that you know what you're doing when examining financial institutions. Not gonna lie, anyone can claim they understand solvency analysis, but having an Accredited Financial Examiner credential proves it.

Recognition matters. These credentials get recognized across state and federal regulatory agencies, which is huge because if you work for the Texas Department of Insurance and want to move to North Carolina's insurance department, they know exactly what your AFE certification means. If you're applying to the FDIC or OCC, they respect these credentials because they're specific to regulatory examination work. Not some generic business certification that could mean anything.

Here's what matters for your career: many regulatory positions either require or strongly prefer SOFE certifications. Some states won't promote you past certain levels without them. The continuing education requirements also keep your knowledge current, which honestly is necessary given how fast the financial world changes. What worked last year might be obsolete now.

The 2026 regulatory environment

Financial services regulation's getting more complex every single year. We're not just looking at traditional risks anymore. Now examiners need to understand cybersecurity threats, fintech business models, and ESG factors that didn't exist when a lot of current examiners started their careers.

The demand for qualified financial examiners is growing because of this complexity. State insurance departments are competing with each other and with federal agencies for talent. Having SOFE certifications gives you job security that a lot of industries don't offer right now. The thing is, you can't just hire someone off the street for these roles anymore. The technical knowledge required has exploded.

Competitive advantage matters too. In government regulatory roles, certifications can mean higher pay grades and faster promotions. In private sector compliance roles at insurance companies or banks, showing you understand examination from the regulator's perspective makes you way more valuable. Like speaking their language fluently.

Remote examination capabilities have transformed how regulatory work happens. The pandemic accelerated this, but it's permanent now. Examiners conduct virtual desk examinations, analyze data remotely, and use digital tools that didn't exist five years ago. SOFE's certification content has adapted to these changes, which keeps the credentials relevant instead of turning into outdated relics nobody respects.

What these exams actually cover

Wide range here. SOFE certifications cover plenty of financial institutions. Insurance companies are the big one: life insurance, health insurance, property and casualty carriers. Each type has different risk profiles and regulatory requirements that examiners need to understand.

Banks and credit unions fall under this umbrella. Investment firms and broker-dealers too. Pension funds and retirement systems, which is a whole specialized area because you're dealing with people's retirement security. Talk about high stakes. Healthcare organizations and managed care entities, where financial solvency intersects with healthcare delivery. Captive insurance companies and risk retention groups, which are niche but important.

The breadth is actually one reason these certifications matter. You're not just learning theory, you're learning practical application across different institution types. Real-world stuff.

Who benefits from SOFE credentials

State insurance department examiners? Obvious candidates. If you work for a state regulator, these certifications are often part of your career progression. Non-negotiable, really.

Federal regulatory agency employees at the FDIC, OCC, or Federal Reserve also pursue these. The focus on financial condition assessment and solvency analysis translates across different types of institutions. Makes the credentials versatile even though they're specialized. Kinda paradoxical, but it works.

Internal auditors in financial institutions benefit because understanding regulatory examination helps them prepare their companies for exams and identify issues before regulators do. Risk management professionals and compliance officers use these credentials for similar reasons. Like insider knowledge.

Career changers entering financial regulation from accounting or general finance find SOFE certifications helpful for establishing credibility quickly. Recent graduates in finance, accounting, or economics can use them to differentiate themselves when applying for entry-level regulatory positions. Standing out's tough otherwise.

How SOFE credentials differ from other designations

Different focus entirely. The CPA focuses on accounting and auditing broadly. The CFA is about investment analysis and portfolio management. The CFE (Certified Fraud Examiner) concentrates on fraud detection and prevention. SOFE certifications zero in on regulatory examination and solvency analysis.

This specialization is the whole point. You're learning examination procedures and protocols that regulators actually use. How to review an insurance company's reserves. How to assess a bank's capital adequacy. How to identify red flags in financial statements that indicate deteriorating financial condition. The stuff that keeps regulators up at night.

These credentials work alongside those other designations, not against them. I know plenty of people who have both a CPA and an AFE certification. They serve different purposes. Honestly, the combination makes you pretty formidable.

Cost and time commitment are also factors. SOFE certifications generally require less preparation time than a CPA or CFA and cost less. That doesn't make them easier or less valuable, just more focused. You're not studying tax code for three months when you'll never use it.

The regulatory forces creating demand

Changed everything. The 2008 financial crisis changed everything about financial regulation. Post-crisis reforms expanded regulatory requirements and scrutiny across the board. Nobody wants another meltdown.

The United States has a state-based insurance regulation system, which is kind of unusual globally. Each state has its own insurance department. The National Association of Insurance Commissioners (NAIC) sets accreditation standards that states must meet. These standards require qualified examiners, which drives demand for SOFE certifications. Baked into the system.

The Dodd-Frank Act created new requirements and regulatory structures. Implementation is ongoing even now, years later. Bureaucracy moves slow, you know? Financial products and structures keep getting more complex: derivatives, reinsurance arrangements, alternative risk transfer mechanisms. It's a lot.

Cross-border regulatory coordination matters more as financial institutions operate globally. International standards like Solvency II in Europe influence U.S. practices. Examiners need to understand these frameworks, and SOFE education helps with that. The financial world's interconnected now whether we like it or not.

Honestly, if you're considering a career in financial regulation, SOFE certifications are one of the smarter investments you can make in your professional development. They're targeted, respected, and increasingly necessary.

SOFE Certification Paths: From Beginner to Advanced

SOFE certification exams overview

SOFE Certification Exams work like a progression system. They're built for people working in financial and insurance examination, usually regulators or supervisory teams, sometimes the folks who back them up operationally. You've got people jumping in from accounting backgrounds wanting something structured to follow, and then there's the crowd already neck-deep in examination work who suddenly need it because, well, HR made it mandatory. Both scenarios play out constantly.

Here's the thing: it's designed as a ladder. You begin at Associate level, show you've got the vocabulary down, then gradually work into heavier analytical stuff, niche specializations, and if you stick with it long enough, leadership territory. Small jumps. Defined milestones. Credentials that actually register with hiring managers when they're skimming resumes.

what SOFE is and what these certifications cover

SOFE certifications basically mirror what examiners actually do day-to-day: digging through financial statements, evaluating capital and surplus positions, decoding statutory reporting requirements, identifying risk exposures, documenting what you find, and (this matters more than people admit) communicating problems without accidentally triggering organizational chaos. That diplomacy piece? Real skill.

Content-wise, expect foundational accounting principles, regulatory frameworks, examination planning mechanics, workpaper standards, professional ethics. At advanced tiers it gets trickier and more subjective, because now you're interpreting warning signs instead of just transcribing figures.

I once watched a senior examiner spend forty minutes explaining to a CFO why their reserve methodology looked fine on paper but created exposure they hadn't considered. The CFO kept insisting their actuary signed off on everything. Eventually the examiner just asked, "If rates moved 200 basis points tomorrow, would you feel comfortable with these assumptions?" Silence. That's the kind of thinking these certifications try to develop, though honestly no exam fully prepares you for those moments.

beginner path: entry-level certifications for newcomers

Brand new? The Associate Financial Examiner (AFE) is your starting line. People Google it as the SOFE AFE exam, and yeah, I'd absolutely recommend it first if you've got under two years of examination exposure and want a legitimate financial examiner credential without overselling your experience level.

AFE teaches the procedural stuff. Not flashy. Extremely marketable.

Eligibility? Usually you're good if you can demonstrate basic education or some relevant job history, plus you satisfy the SOFE certification requirements they publish for AFE candidates. Rules shift slightly with program updates, but the core logic stays consistent: AFE is deliberately accessible early on, with prerequisites that don't assume you've been authorizing exam scopes for half a decade. Think of it as the launchpad for the AFE certification path even if your long-term aim is insurance specialization or management.

Time investment? Most people I've watched succeed without major drama spend 2 to 6 weeks studying consistently, though background matters heavily. Recent accounting experience accelerates things. Coming from operations or a non-finance function? Budget extra time and lean harder on practice materials. The AFE exam preparation guide you assemble is more critical than sheer hour count.

AFE exam format, domains, and what you're expected to know

AFE content casts a wide net intentionally. You're demonstrating baseline competence.

Standard coverage includes financial reporting fundamentals, examination planning and documentation practices, regulatory concepts, ethics requirements, foundational analytical techniques. The AFE exam objectives push you toward understanding what examiners prioritize, how conclusions get supported with evidence, and what constitutes "adequate documentation" in workpapers.

Three pitfalls catch candidates repeatedly. Terminology confusion. Calculation errors from rushing. Poor reading discipline under time pressure.

That's why I advocate working SOFE AFE practice questions early in your prep cycle, not as a panic move the final week. You want blind spots exposed while there's runway to address them, and quality AFE exam study resources typically feature scenario-based questions that replicate the judgment calls you'll encounter professionally.

career positions that fit AFE holders

AFE works perfectly for entry-level positions where you're contributing to exams, constructing workpapers, or handling defined analytical segments under supervision. Job titles like examiner trainee, junior financial analyst within regulatory environments, examination associate, compliance support roles intersecting with filings and statutory reporting.

And yes, compensation questions surface constantly. AFE certification salary impact exists, though it's contextual and messy. Some organizations treat it as a promotion prerequisite checkbox. Others attach a modest pay adjustment plus access to more substantive assignments. The more valuable aspect is the SOFE certification career impact on professional credibility when you're transitioning from support functions into owning exam sections independently.

For a direct reference point, here's the AFE resource I consistently share: AFE (Accredited Financial Examiner). Use it to structure your approach, not circumvent the actual learning process.

intermediate options: moving from AFE to CFE

Post-AFE, the logical progression is the Certified Financial Examiner (CFE) designation. This is where expectations shift. The program now assumes you've cycled through actual examinations multiple times and understand how unpredictable and incomplete data typically is in practice.

Experience benchmarks at this tier usually fall around 3 to 5 years. Not always rigidly enforced, but that's the implicit expectation. You're moving beyond "I can execute templates" into "I can contextualize these figures, articulate the risk implications, and recommend appropriate examiner responses."

Subject matter sharpens considerably. More sophisticated analysis. Stronger connections between financial performance and underlying risks. Greater emphasis on documentation quality and defensible conclusions that withstand scrutiny during review cycles. If you're curious about SOFE exam difficulty ranking, I'd position AFE as the access point, CFE as the first genuine filter, and advanced credentials as the "professional maturity required" category.

Career alignment? CFE typically maps to examiner roles where you independently manage substantial exam components, help with stakeholder meetings, author significant report sections, and justify your conclusions when senior reviewers probe with uncomfortable questions. Which happens. Frequently.

advanced and specialized: CIE and CSFE

At the upper tiers you're choosing between specialization and leadership tracks. Two primary destinations:

Certified Insurance Examiner (CIE) targets professionals diving deep into insurance-specific examination complexities. Statutory reporting details, reserving methodologies, product risk assessment, reinsurance mechanics, market conduct knowledge. The specialized content that makes generalist finance people uncomfortable. If your trajectory centers on insurance supervision, CIE broadcasts credibility.

Certified Senior Financial Examiner (CSFE) represents the senior designation aligned with team leadership, exam program management, and decision-making under ambiguity. Leadership and management competencies emerge here alongside complex analytical work and enterprise risk assessment. You're not merely executing work. You're reviewing others' output, coaching team members, establishing strategic direction. That covers supervisory capabilities, team coordination, strategic planning, occasionally even regulatory policy development. Organizational politics included, I mean it.

which SOFE exam should you take first

Start with honest self-evaluation. What do you really understand versus what you vaguely recognize. Massive difference.

Then align it with career objectives and realistic target roles. Pursuing an examiner career path early on? AFE first, no question. Already performing examiner-level responsibilities with documentation to prove it? You might explore accelerated options, but skipping foundational material backfires because subsequent exams assume you've internalized basics thoroughly, not just memorized enough to pass.

Also verify employer specifications. Some agencies mandate particular sequencing. Time availability factors in because rushing this material is a common failure pattern, and yes, budget realistically for exam fees plus preparation materials. Financial constraints are real. Always.

Finally, confirm current prerequisites and sequencing protocols. Don't make assumptions. Review published requirements before committing financially.

recommended progression pathways (and realistic timelines)

Traditional sequence is straightforward: AFE, then CFE, then CIE or CSFE. For most professionals, that represents a 1 to 5 year timeline depending on workplace exposure intensity and testing pace.

Accelerated pathway suits experienced professionals transitioning from audit, accounting, or regulatory backgrounds where they've already performed comparable analytical work. They may condense timelines, but prerequisite requirements and continuing education obligations still apply.

Specialized tracks develop organically. Insurance concentration naturally pushes toward CIE. Banking or broader financial examination focus typically maintains CFE alignment before CSFE. Between certifications, anticipate continuing education mandates. And maintaining multiple active credentials simultaneously is feasible, just administratively annoying, because CPE tracking becomes its own parallel workstream.

stacking SOFE certifications with other credentials

People obsess over credential stacking. Sometimes strategic, sometimes just résumé decoration.

CPA complements nicely if your work emphasizes financial reporting and you need immediate credibility with accounting-centric stakeholders. CISA fits when your environment includes technology risk and systems controls, particularly where financial reporting depends on complex IT infrastructure. CIA suits audit professionals building a cohesive audit-to-examination career narrative.

Let me break down two common combinations. First, CPA plus SOFE creates a powerful pairing when targeting senior analytical or review positions, because CPA signals deep accounting expertise while SOFE demonstrates examiner methodology fluency. Second, CFE (fraud examination) plus SOFE can unlock unique opportunities if your assignments involve investigations or you routinely identify anomalies that organizations hesitate to explicitly label as fraud.

CFA adds value too, though it skews toward investment analysis orientation. Helpful, just not always directly applicable.

renewal, CPE, and staying certified

Recertification cycles and deadlines are where motivation collapses. Calendar the dates immediately. Seriously.

CPE requirements typically accommodate conferences, seminars, approved training programs, self-study modules, or online courses. SOFE conferences offer efficient credit accumulation, but self-study often rescues you when work demands spike unexpectedly. Document everything contemporaneously, preserve completion certificates, and absolutely don't wait until deadline month attempting to reconstruct your activities from scattered email confirmations.

international recognition and reciprocity

SOFE certifications carry weight internationally, particularly where regulators value structured examiner development programs and where alignment with organizations like the International Association of Insurance Supervisors (IAIS) shapes professional expectations. Recognition varies by jurisdiction and specific agency, so don't presume automatic reciprocity, but Canadian and various foreign regulators generally understand what these designations represent regarding professional competence.

Cross-border opportunities exist. Global standards are gradually converging. Credentials help, but practical experience ultimately matters most.

quick AFE FAQ style answers people ask

What is the SOFE AFE certification and who should take it? AFE is the foundational credential for early-career examiners and adjacent professionals needing grounding in examiner practices and financial fundamentals.

How hard is the AFE exam compared to other SOFE certification exams? It's the most accessible in the progression, but still trips up candidates who skip practice questions or underestimate the scenario-based and reading comprehension components.

What is the best study plan and resources for the AFE exam? Begin with published objectives, then integrate official references with targeted practice question sets, and systematically review mistakes weekly. If you need a central resource, start with AFE (Accredited Financial Examiner) and expand outward.

What jobs can I get with an Accredited Financial Examiner certification? Entry-level examiner positions, trainee roles, exam support analyst functions, compliance positions interfacing with filings and regulatory reporting.

What salary increase can I expect after earning the AFE certification? Depends on agency compensation structures, geographic location, and whether it triggers promotion eligibility, but the more significant benefit is access to higher-quality assignments that compound into senior-grade positions over time.

Accredited Financial Examiner (AFE) Certification: Complete Exam Guide

Understanding the AFE credential in regulatory finance

The Accredited Financial Examiner certification gets you into state insurance regulation. It's the foundational credential from the Society of Financial Examiners (SOFE), built for folks examining insurance companies on behalf of state regulators. This isn't your CFA or CPA situation. Way more niche. Focused on the actual regulatory work you'll tackle when you're sitting at your desk trying to figure out if some insurance company's balance sheet is hiding problems.

This certification proves you know the basics: financial examination principles, statutory accounting, and that regulatory framework governing insurance companies. State insurance departments nationwide recognize it as baseline competency. Starting out as a financial examiner? This is your ticket in. Shows you're committed to regulatory work and not just killing time until something better comes along.

The AFE sits at the bottom of SOFE's certification ladder. That's fine, though. We all start somewhere. It's your launchpad before tackling beefier credentials like the CFE (Certified Financial Examiner) or AIE (Accredited Insurance Examiner).

Who actually needs this certification

New hires? Absolutely.

State insurance departments target fresh graduates. Just finished college? You're the demographic. Most state departments expect new financial examiners to snag the AFE within year one or two on the job. Some states literally won't let you conduct examinations solo until you've cleared it, which makes sense when you think about the responsibility involved.

Career changers jumping into financial examination from corporate finance or internal audit should look at this. Maybe you've spent years crunching numbers in a different environment and want the regulatory angle. The AFE delivers that foundation you're missing. GAAP accounting and statutory accounting? Completely different beasts, and this exam drills you on the statutory framework that insurance regulators actually care about.

Compliance professionals expanding their skillsets find value here too, particularly if they're embedded in insurance companies wanting to understand the examiner's mindset. Financial analysts in regulatory agencies, internal auditors seeking regulatory chops. Basically anyone touching insurance regulation from any direction gets something out of this.

Most positions demand a bachelor's degree minimum. Some states flex on the major, but finance, accounting, or business administration obviously align better with the content.

Getting eligible and meeting the requirements

You'll typically need that bachelor's degree or comparable experience to sit for the exam. Work experience requirements are surprisingly chill compared to other certifications, usually landing in the 0-2 year range, though plenty of candidates tackle it with zero experience during their onboarding phase.

SOFE membership is required for exam eligibility, which delivers benefits beyond just letting you test. You gain access to their professional network, conferences, and educational resources that support your entire career trajectory. The application process involves documentation of your education and paying registration fees. Exam registration costs a few hundred bucks, plus you'll want to budget for study materials that don't come cheap.

Background checks are standard procedure since you're entering a regulatory role handling confidential financial information that could move markets if leaked. Character requirements exist but aren't crazy strict. They mainly verify you don't have a history of financial crimes or ethical violations compromising your objectivity as an examiner, which seems like a reasonable bar.

Retest policies let you attempt the exam multiple times if needed, though waiting periods exist between attempts and you'll fork over that exam fee again.

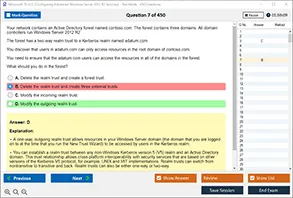

The exam format and what to expect on test day

Typically 100-150 multiple choice questions populate the AFE exam. Exact count varies depending on which version you get. You're allocated 3-4 hours to complete it, which sounds generous but evaporates fast when you're parsing scenario-based questions demanding actual analysis rather than simple recall.

It's administered through computer-based testing at designated centers. Some candidates get remote proctoring options, which beats driving two hours to the nearest testing center if you're in a rural area. The CBT interface is pretty straightforward, nothing flashy, just questions and answer choices. You can flag questions for later review and work through backward and forward through the exam.

Question types include straightforward multiple choice and scenario-based situations where you're handed a case and asked to apply your knowledge under pressure. The scenarios often involve dissecting financial statements or determining the appropriate regulatory response to a particular circumstance that doesn't have an obvious answer.

Scoring uses scaled methodology, and you'll get preliminary results immediately after finishing. Official score reporting comes later, but at least you know right away whether you passed or need to regroup. The passing standard is set through psychometric analysis, so it's not a simple percentage that changes based on exam difficulty.

Breaking down the content domains

Financial statement analysis fundamentals

This domain eats up 25-30% of the exam and covers balance sheet components, income statement interpretation, and cash flow statement evaluation in ways that actually matter for regulatory work. You need to understand statutory financial statements specifically, not just those general GAAP statements they taught in college. Financial ratios and benchmarks are massive here, covering liquidity ratios, use ratios, profitability measures that signal whether a company can pay claims. Trend analysis techniques help you spot red flags emerging over multiple reporting periods before they explode into insolvency.

Regulatory structure and framework

About 20-25% of questions test your knowledge of how state insurance regulation actually functions in the real world, not textbook theory. The NAIC model laws and regulations form the foundation, though each state can adopt or modify them based on local politics and priorities. You'll need to understand federal oversight coordination, regulatory authority limits, and examination standards. This material sounds dry as toast but it's actually the backbone of everything you'll do as an examiner, determining what you can and can't force companies to do.

I remember my first week on the job, getting handed a three-inch binder of NAIC guidelines and thinking it was some kind of hazing ritual. Turns out you actually need most of that stuff. Not all at once, thankfully, but you'll reference different sections constantly depending on what you're examining.

Risk assessment approaches

Another 20-25% focuses on identifying financial risks and deploying the risk-focused examination approach that's become industry standard over the past decade. Materiality determination is critical. You can't examine every single transaction, so you need to know what's significant enough to warrant attention and what you can reasonably skip. Risk categorization, early warning systems, financial ratios triggering regulatory concern are practical skills you'll use constantly, not abstract concepts.

Examination procedures and methodology

15-20% covers the nuts and bolts of actually conducting examinations without screwing up. Planning and scoping, documentation standards, sampling techniques, testing procedures, report writing that holds up under legal scrutiny. The workpaper standards are particularly critical because poorly documented work can undermine an entire examination. I've seen examiners have to redo weeks of work because their documentation didn't meet standards and the company's lawyers tore it apart.

Insurance operations knowledge

10-15% tests your understanding of how insurance companies actually operate beyond the financial statements. Types of products, underwriting principles, claims processes, reinsurance fundamentals that shift risk around the industry. You don't need to be an underwriter yourself, but you need enough knowledge to understand what you're examining and whether it makes business sense.

Professional ethics requirements

The smallest domain at 5-10%, but don't sleep on it. Examiner independence, confidentiality, conflicts of interest aren't theoretical concepts you discuss in philosophy class. Violating ethical standards can torpedo your career in regulation permanently, creating a reputation you'll never shake in this tight-knit industry.

Critical topics that appear throughout

Statutory accounting principles versus GAAP? Probably the single most key conceptual difference you need to master cold. SAP is conservative and focused on policyholder protection, making sure companies can pay claims even in worst-case scenarios, while GAAP aims for matching and accurate profit reporting that makes investors happy. The annual statement structure, that infamous "yellow book," is something you'll reference constantly throughout your career until you can work through it blindfolded.

Risk-Based Capital formulas and ratios determine exactly when regulators need to intervene in a company's operations, from gentle suggestions to full-blown takeovers. Understanding how RBC is calculated and what the different action levels mean is critical knowledge. The AFE exam tests this thoroughly because it's so fundamental to solvency regulation that you literally can't do the job without it.

NAIC Financial Analysis Handbook guidance provides detailed procedures for analysis that go way beyond what you learned in school. Market conduct examination versus financial examination distinctions matter because they're completely different types of regulatory work with different objectives, different teams, different skillsets required.

How AFE compares to other entry-level credentials

Night and day difference, really.

The specific focus on regulatory examination sets it apart from general finance certifications teaching you portfolio management or investment strategies. You're not learning how to maximize shareholder value. You're learning how to examine insurance companies for solvency and compliance, protecting policyholders who have no idea what's happening behind the scenes. The practical application to government regulatory work means everything you learn directly applies to your job rather than being theoretical knowledge you might use someday.

The focus on statutory accounting versus GAAP is really unique. Most finance certifications teach GAAP exclusively because that's what corporations use. The solvency analysis and consumer protection orientation reflects the regulatory mission rather than profit maximization, which requires a completely different mindset. State-based regulatory system knowledge is something you won't get from national certifications designed for corporate finance roles.

Cost-wise, it's way cheaper and faster than pursuing a CPA or CFA that'll drain your bank account and consume years of your life. You can realistically prepare and pass within a few months while working full-time and maintaining some semblance of a personal life. For public sector career paths, it's directly relevant in a way that other certifications aren't.

Difficulty assessment and realistic expectations

Historical pass rates typically run 60-75% for first-time takers, which is pretty reasonable compared to some professional exams with 40% pass rates designed to gatekeep the profession. The exam is challenging but definitely passable with proper preparation and a solid study plan you actually stick to. Common challenging topics include statutory accounting differences that contradict everything you learned in college, RBC calculations with their endless formulas, and the details of regulatory authority and examination procedures that vary by jurisdiction.

Compared to other professional certification exams? Less brutal than the CPA exam that destroys souls, but more challenging than some entry-level IT certifications you can pass by watching YouTube videos. Candidates with accounting backgrounds generally find it easier than those coming from economics, political science, or other disciplines without that foundation. Retake rates are moderate. Most people who fail once pass on their second attempt after targeted study addressing their weak areas.

Study time correlation with pass probability is absolutely real and backed by data. Candidates who dedicate 40-60 hours of focused study time have significantly higher pass rates than those who cram for a week thinking they can wing it based on work experience. The material requires genuine understanding, not just memorization of formulas, so you need time for concepts to actually sink in and connect.

AFE Certification Career Impact and Professional Opportunities

where AFE sits inside SOFE Certification Exams

The SOFE Certification Exams ecosystem is basically a ladder. AFE is the first real rung that hiring managers recognize as more than "I took a class once." It's the credential that says you can read regulated financials, follow examiner guidance, and not fall apart when someone hands you a stack of workpapers and says "document your conclusion."

Real talk here.

AFE also works as a foundation for the advanced SOFE credentials, and that part matters if you want this to be a career instead of a stopover. The thing is, the AFE certification path gets treated as the entry point into a regulatory examination career. In a lot of shops it's the informal (or formal) prerequisite before you're considered for CFE and other specialized certifications. AFE proves you can handle the baseline examiner toolkit before you move into tougher scopes, heavier judgment calls, and more exposure to accreditation-driven work.

Baseline competency. That's the phrase.

Not gonna lie, employers like it because it reduces uncertainty. If you passed the SOFE AFE exam, they assume you can be trained faster, you'll make fewer avoidable documentation mistakes, and you'll understand why controls, governance, and regulatory standards aren't "optional suggestions" when a department's defending decisions in public records.

AFE as the first "real" career building block

AFE builds career progression, and it shows initiative in a way that random coursework doesn't. You're basically telling an employer, "I can learn structured material, I can pass a proctored exam, and I'm sticking around long enough to justify the investment." That last part? Huge in government roles where teams are chronically understaffed and training cycles drag on forever.

It also opens doors for on-the-job training opportunities. A lot of agencies will rotate newer staff through exam roles, analysis, and compliance support, but they're way more willing to put you on a live exam if you've already proven you understand the basics of statements, ratios, and documentation standards. The work gets reviewed, archived, and sometimes fought over.

Paper trail. Always.

And yes, AFE's frequently treated as a prerequisite for CFE and specialized certifications. Even when it's not written as a hard requirement, it becomes the "default path" managers expect. That's why you'll see teams map development plans around AFE first, then the next credential when you've got a couple exam cycles under your belt.

roles you can realistically land with AFE

If you're asking "What jobs can I get with an Accredited Financial Examiner certification?" the honest answer is that it unlocks the first tier of roles where you're trusted to touch regulated financial work with supervision, not just admin support.

Financial Examiner I/II

Classic outcome here. You'll see Financial Examiner I and II postings where AFE's required or preferred, especially for entry-level examination staff roles. Day to day, that looks like participation in examination teams, workpaper preparation and documentation, basic analytical assignments, and the kind of "go verify this number back to source" tasks that sound boring until you realize they're how you learn what good evidence looks like.

You'll also get exposure to exam planning support and risk scoping, even if you're not the one making final calls. Starting salary ranges? Commonly $45,000 to $65,000, and yes, location and union structures swing that number a lot, but the AFE certification salary conversation usually starts there.

Associate Insurance Analyst

This role leans more into monitoring and analysis than field exam work. Think quarterly statement review, ratio work, trend spotting, and support for senior analysts who are deciding what needs follow-up. You're not "running the show," but you're producing the work that informs what the show even is.

More spreadsheets. Better questions.

Junior Compliance Officer

If you're compliance-inclined, AFE helps because you already speak the language of regulatory expectations. Junior compliance work's often regulatory monitoring, policy and procedure review, internal audit support, and documentation. The main skill shift? Learning internal operations and controls, not just external reporting.

Risk Assessment Specialist

This is the role that surprises people, honestly. AFE can translate well into risk identification, data collection, risk rating assignments, and examination planning support. Risk work loves structured thinking and hates hand-wavy conclusions. You'll still need to learn the organization's risk framework, but you won't be starting from zero.

Other roles exist too, like exam coordinator, audit associate, or regulatory reporting analyst, but the four above are the most straightforward.

who hires AFE holders and where the demand shows up

This isn't a niche credential that only one type of employer cares about. You'll see demand across:

State insurance departments (all 50 states plus territories), which is the most direct path into examiner work. Federal regulatory agencies like FDIC, OCC, and the Federal Reserve, especially if your skill set overlaps with financial condition review. NAIC, where standards and accreditation expectations influence what state departments prioritize. Insurance companies doing internal audit and compliance, because they like hiring people who think like examiners. Consulting firms specializing in regulatory services, third-party examination contractors, and government accountability offices.

Honestly, the employer list's broad because regulated financial review is a transferable skill. It's not glamorous, but it's portable. I know someone who started in a state insurance department, moved to a Big Four consulting practice doing regulatory work, then landed at a Fortune 500 insurer running internal controls. AFE was on every application.

what changes after AFE: promotions, scope, and timeline

Career advancement post-AFE's usually pretty predictable if you perform well. Typical timeline to advancement is two to four years, and that's not magical. It's basically "enough cycles" to show you can handle more independence.

Promotions often look like moving to senior examiner positions, then supervisory and team lead roles. After that, you start getting specialized examination assignments for complex entities, more involvement in policy development and regulatory drafting, and training responsibilities. If you like management, there's a management track, and government structures usually make the path clear even if the pace is slow.

Some people hate that structure. I like it.

skills you build while studying and using AFE

AFE isn't just a line on a resume. The competency list's pretty practical:

Financial statement analysis proficiency, especially regulated statements and what the numbers imply. Regulatory knowledge and interpretation, which is basically "read rules, apply rules, document why." Risk assessment and critical thinking, because you're constantly deciding what matters and what is noise. Professional communication, written and verbal, since your workpapers and summaries need to survive review. Attention to detail, because tiny errors become big issues in regulated work. Ethical judgment, because you'll see sensitive information and gray areas. Time management, since exam timelines are real and people are waiting on your section.

The best part? These skills compound. Once you learn to document conclusions cleanly, every future role gets easier.

AFE recognition, hiring advantage, and why it helps in competitive markets

You'll find job postings requiring or preferring AFE, and that's the simplest form of demand. The more subtle version is competitive advantage in hiring processes, because certification signals career seriousness and longevity, and agencies care about retention.

It also reduces employer training costs and time. Faster onboarding and productivity isn't a "nice to have" when teams are short staffed. Plus, AFE can increase credibility with examination subjects, because you're not just a new hire with a badge. You're a new hire with a financial examiner credential that implies shared standards and vocabulary.

Money matters too. Many employers have tuition reimbursement and support programs, and some state department policies actively encourage certification. NAIC accreditation standards also tend to nudge departments toward staff development, which is why certifications keep showing up in internal performance plans.

long-term trajectory: 5, 10, 15+ years

Five years out, a lot of AFE holders are senior examiners or specialists. Ten years out? Supervisory or management positions are realistic if you want them and you're good at people work, not just technical work. Fifteen-plus years can put you into executive leadership opportunities, especially in public sector regulatory roles where institutional knowledge gets valued.

Alternative paths exist. Consulting's common, private sector compliance is common, and some folks go into training or academia.

Geographic mobility helps too. Many skills transfer across states and territories, and government regulatory roles tend to offer stability, pension and benefits, and predictable progression if you're consistent.

professional development and networking through SOFE

SOFE isn't only exams. The networking's part of the value, especially early on when you don't know what "good" looks like yet.

You'll see annual career development seminars, regional meetings and workshops, online communities, mentorship programs connecting new and experienced examiners, job boards, continuing education opportunities, and leadership development programs. You can ignore all of that and still pass tests, but you'll grow faster if you show up and talk to people who've been on the hard exams.

quick notes on prep, difficulty, and resources

People ask about the SOFE exam difficulty ranking and where AFE sits. It's not the hardest in the catalog, but it's also not a "skim a PDF" situation if you're new to regulatory statements and examiner documentation. Most failures come from underestimating how specific the AFE exam objectives can be, and from not practicing how questions get asked.

If you're looking for an AFE exam preparation guide, start with the published objectives, then build a plan around weak areas, then grind practice. AFE exam study resources that include scenario questions help more than pure memorization, because the exam wants application. Also, do timed sets. Pressure changes everything.

For targeted prep and SOFE AFE practice questions, the AFE page is here: AFE (Accredited Financial Examiner).

AFE Certification Salary Impact and Compensation Analysis

What AFE certification actually pays across different examiner roles

Okay, so here's the deal. The salary ranges for AFE certification holders? They're all over the place depending on where you land and what level you're at. Entry-level financial examiners with their fresh AFE certification typically pull in somewhere between $45,000 and $65,000 annually, which isn't bad for starting out in government work, though I've got mixed feelings about whether that's actually competitive with private sector opportunities when you factor in student loans and cost of living in cities where these jobs tend to cluster.

State department positions? Total chaos. You might start at $48,000 in Tennessee but need $62,000 just to maintain the same lifestyle in Massachusetts because cost of living differences are absolutely real and nobody warns you about this stuff in school. Federal agency starting salaries follow the GS scale pretty religiously. We're talking GS-7 to GS-9 range for new AFE holders, which translates to roughly $47,000 to $60,000 depending on your locality adjustment. Geographic variation matters more than most people realize when they're comparing offers, I mean really comparing them beyond just the number on the offer letter.

Once you've got that AFE certification and 1-3 years under your belt, you're looking at Financial Examiner II territory. That's $55,000 to $75,000, give or take. The jump comes from increased responsibility and handling more complex examinations. You're not just checking boxes anymore, you're actually analyzing financial institutions with some autonomy and making judgment calls that matter. Performance-based increases can push you toward the higher end faster if you're good at what you do and your supervisor actually notices.

Senior financial examiners with 3-5 years experience and maybe some additional certifications beyond AFE? They're commanding $70,000 to $95,000, which honestly feels about right for the responsibility level. At this level you're leading examinations, mentoring newer examiners, and getting those specialized assignments that actually matter. Wait, I should mention that mentoring responsibility doesn't always come with extra pay even though it absolutely should. Anyway, you're the person they call when something complicated comes up.

Supervisory roles change everything. We're talking $85,000 to $120,000 for managing teams, developing policy, and handling the development of other examiners. it's about examination work anymore. You're running the show for your unit and dealing with personnel issues and budget constraints.

The real difference certification makes to your paycheck

Here's what actually happens to your earning potential when you get the AFE, and it's not always what people expect. Pre-certification entry-level positions in financial examination hover around $40,000 to $55,000. Post-certification? You're starting at $45,000 to $65,000. That's an immediate salary increase averaging 8-15% just for having those three letters after your name, which sounds great until you realize how much the exam costs and how many study hours you invested.

But here's the thing. The real value isn't that initial bump. It's the faster promotion trajectory that increases your lifetime earnings substantially over decades, not just the first year or two. You qualify for positions that non-certified examiners simply can't access, and you move through pay grades quicker because you've demonstrated professional competency through SOFE certification exams.

Better negotiation use? Totally underrated. When you walk into a salary discussion with AFE certification, you're not asking for more money based on potential. You're proving you've already met a recognized industry standard that your employer values and maybe even requires for certain positions.

Government scales make this especially clear since certification often qualifies you for higher pay grades automatically, though the bureaucracy around actually getting reclassified can be frustrating.

Geographic realities nobody talks about enough

High-cost states like California, New York, and Massachusetts add a 20-40% premium to those baseline salary ranges, but it never feels like enough when you're actually living there. A senior examiner making $70,000 in North Carolina might need $90,000 in San Francisco just to break even on housing costs alone, and that's not even considering the tax differences between states or the reality that $90,000 still means roommates in some Bay Area neighborhoods. My cousin moved out there thinking she'd struck gold with a $95,000 offer until she saw what apartments actually cost and realized she'd been better off financially in Charlotte.

Mid-cost states like Texas, Florida, and North Carolina represent the baseline ranges I've been quoting throughout this analysis.

Low-cost states (Mississippi, Arkansas, Oklahoma) typically run 10-20% below baseline, which sounds bad until you realize that $65,000 entry-level position might be $54,000 in rural Arkansas but your rent is also $600 instead of $2,200 and you're probably not stuck in traffic for two hours daily. Metropolitan versus rural differences exist even within the same state, which complicates things when you're comparing offers across regions or trying to figure out where you'll actually have the best quality of life.

Experience compounds with certification

Entry-level examiners with 0-2 years sit in the lower quartile of pay ranges, as you'd expect. Mid-career professionals with 3-7 years hit median ranges pretty consistently across most states and agencies. Experienced examiners with 8+ years reach upper quartile compensation, especially when they've specialized in high-demand areas like cybersecurity or complex derivatives.

The AFE accelerates this whole progression. You're not just getting older and more experienced. You're getting promoted faster because the certification opens doors that would otherwise stay closed for another year or two while your non-certified colleagues wait for positions to open up or requirements to change.

Public versus private sector compensation trade-offs

State government offers competitive base salaries with incredibly strong benefits packages that you really can't replicate in most private sector jobs. Federal government follows the GS scale with locality adjustments that can significantly boost your effective compensation in expensive areas, plus job security that's become increasingly valuable in uncertain economic times. Private sector consulting firms typically pay 15-30% higher base salaries for AFE holders because they can bill you out at premium rates to clients who specifically request certified examiners for regulatory work.

Private sector insurance companies are variable but often higher than government positions, though the culture can be dramatically different. I've seen AFE-certified examiners leave state positions for insurance company roles paying $20,000 more annually. The benefits package usually isn't quite as generous and the job security definitely isn't comparable.

Stacking credentials multiplies your value

A master's degree on top of AFE adds about 5-10% to your earning potential, maybe more in federal positions where education levels affect your starting GS grade. The CPA combination is where things get interesting. That's a 15-25% premium because you're bringing two distinct professional certifications that complement each other perfectly and make you incredibly valuable for financial institution examinations. Multiple SOFE certifications can add 10-20% as you demonstrate broader expertise across different examination areas, though honestly the marginal value of each additional cert diminishes somewhat.

Specialized expertise in actuarial work or IT systems can command significant premiums beyond the standard ranges I've been discussing. If you're an AFE holder who also understands insurance company IT infrastructure deeply, you're in rare company and can basically name your price, especially for consulting work.

Total compensation extends way beyond salary

Government pension benefits through defined benefit plans are worth mentioning because they're increasingly rare in the private sector and represent substantial long-term value. Health insurance and healthcare benefits in government roles are typically excellent with low employee contributions. We're talking family coverage for maybe $200-300 monthly that would cost $1,500+ in the private market. Paid time off starts generous and gets better. Fifteen to twenty days annually isn't unusual for newer employees, climbing to 25-30+ days for experienced staff who've accumulated leave over years of service.

Professional development budgets? Check. Tuition reimbursement programs? Often available. Exam fee reimbursement and paid study time? Pretty standard. These all add real value that doesn't show up in your base salary figure but matters tremendously when you're actually living your life. Work-life balance and schedule flexibility matter too, especially if you value actually seeing your family occasionally instead of grinding out 60-hour weeks in consulting.

Career-long earnings trajectory

Years 1-3 typically see 5-8% annual increases as you prove yourself and gain foundational experience. Years 4-7 slow to 4-6% annual increases but you're also hitting promotional opportunities that jump you up significantly beyond standard cost-of-living adjustments. Years 8-15 see 3-5% annual increases with management premiums if you move into supervisory roles, though you're also potentially plateauing unless you keep developing new skills. Years 15+ can reach executive-level compensation potential if you've positioned yourself correctly and haven't burned out, which is honestly a real consideration in regulatory work.

The compounding effect of AFE certification on lifetime earnings is substantial when you actually calculate it out. Conservative estimates put the lifetime earnings premium at $200,000 to $500,000 compared to non-certified career paths, and that's not even accounting for the doors that simply wouldn't open without the credential or the job security advantages during economic downturns.

Regional breakdowns get specific

Northeast region entry-level positions start around $50,000 to $70,000 depending on the specific state and metro area. Southeast comes in at $45,000 to $62,000, which goes further than you'd think in most of those markets. Midwest sits at $43,000 to $60,000, while West Coast pushes $52,000 to $72,000 for the same entry-level work because everything costs more out there. These regional differences persist throughout your career, though they narrow somewhat at senior levels where expertise becomes more valuable than location and you might have more remote work flexibility than entry-level positions typically offer.

Conclusion

Getting ready for your SOFE exam

Look, I'm not gonna sugarcoat this. SOFE certifications aren't the easiest things to tackle. The Accredited Financial Examiner exam especially demands you really understand financial regulation and examination procedures, not just memorize a bunch of terms. But honestly? That's what makes these credentials actually worth something in the real world.

Here's the thing about prep materials, though. You need practice exams that mirror the real format because reading study guides alone won't cut it when you're sitting there staring at scenario-based questions about complex regulatory frameworks that twist your brain into knots. I mean, you can know the material backwards and still freeze up if you haven't practiced applying it under timed conditions. It's weird how that happens, right?

Worth checking out.

The practice resources at /vendor/sofe/ are worth exploring if you're serious about passing (and I assume you are, otherwise why bother?). They've got AFE practice exams at /sofe-dumps/afe/ that simulate actual test conditions, which honestly makes a massive difference in your confidence level when exam day rolls around. I've seen too many people walk into certification exams completely unprepared for the question style and format, then wonder why they failed despite "studying really hard." The thing is, studying and practicing are different things entirely, you know?

Your timeline matters too. Don't try cramming this in two weeks. Give yourself at least 6-8 weeks of consistent study time, maybe more if you're juggling work and life stuff. Block out specific hours each week. Take practice tests regularly. Review what you got wrong because this part's critical, like really critical. Actually understand why you missed those questions instead of just memorizing the right answer for next time.

My cousin tried to cram for his CPA exam in ten days once. Just locked himself in his apartment with energy drinks and flashcards everywhere. Failed spectacularly. Then spent the next three months doing it properly and passed without issue. Funny how that works.

Financial examination is a specialized field and the AFE certification proves you've got the technical knowledge and analytical skills to back up your expertise in ways a resume alone just can't. Whether you're already working in regulatory compliance or trying to break into financial examination roles, this credential opens doors that would otherwise stay locked tight.

Here's what you should do.

So here's what you should do: figure out where you're at knowledge-wise, grab some quality practice materials that don't waste your time, build a realistic study schedule, and commit to the process without making excuses. The exam's challenging but totally manageable if you put in focused preparation time and stay consistent. You've got this, just make sure you're practicing with realistic materials and not just passively reading content like it's a bedtime story. That's the difference between passing and having to retake it, which costs more money and, I mean, nobody wants that hassle.